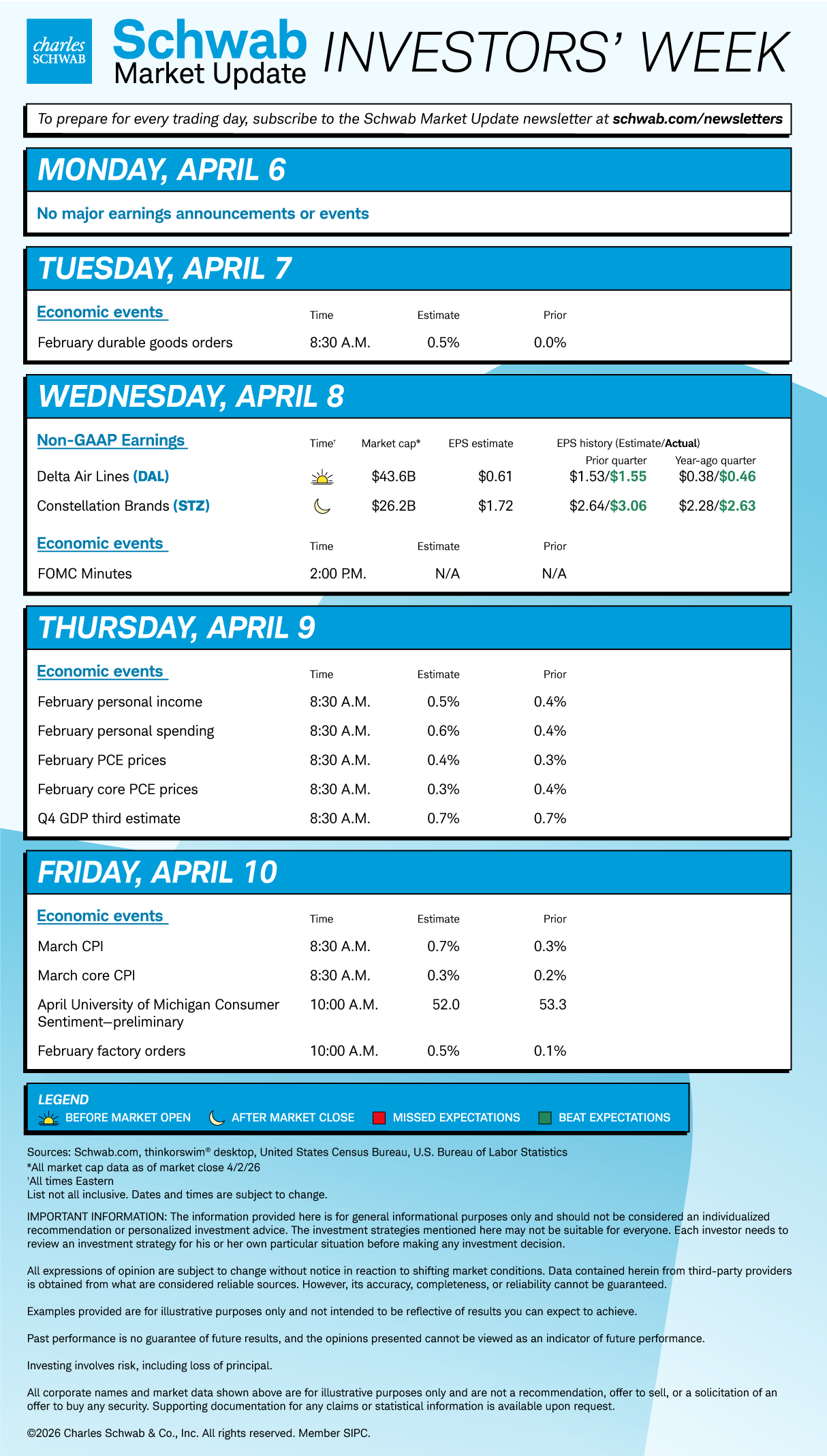

Cautious Optimism to Start Week Despite Firm Crude

Published as of: April 6, 2026, 9:13 a.m. ET

Listen to this update

Listen here or subscribe to the Schwab Market Update in your favorite podcast app.

| The markets | Last price | Change | % change |

|---|---|---|---|

| S&P 500® Index | 6,582.69 | +7.37 | +0.11% |

| Dow Jones Industrial Average® | 46,504.67 | -61.07 | -0.13% |

| Nasdaq Composite® | 21,879.18 | +38.23 | +0.18% |

| 10-year Treasury yield | 4.33% | -0.01 | -- |

| U.S. Dollar Index | 99.87 | -0.15 | -0.15% |

| Cboe Volatility Index® | 24.99 | +1.12 | +4.73% |

| WTI Crude Oil | $110.41 | -1.13 | -1.01% |

| Bitcoin | $69,625 | +$2,490 | +3.71% |

(Monday market open) After snapping a five-week losing streak, major indexes edged up today on fresh ceasefire hopes. Investors approach Monday focused on war news and last Friday's 178,000 rise in March nonfarm payrolls—almost triple what analysts had expected. The market was closed Friday and today is the first full day stocks trade on that report, though there could be distractions as four astronauts fly around the moon for the first time since 1972.

Despite media reports that the U.S. and Iran have received a ceasefire plan, Treasury yields are flat and crude remains elevated near $110 per barrel, possibly weighing those reports with yesterday's threats from President Trump and his deadline of late Tuesday for Iran to re-open the Strait of Hormuz. Oil's persistent gains also put this week's inflation reports front and center. The Federal Reserve's favored Personal Consumption Expenditures (PCE) price index is due later this week, along with minutes from the Fed's last meeting. Before that, Trump holds a news conference at 1 p.m. ET today that could command attention for any new war tidings.

Major indexes climbed Thursday before the jobs data, making last week the first to finish positive since February. That day's rebound from early losses marked one of the first sessions since the war where stocks rose along with oil instead of being repelled by crude's rally. "I’m still not sure that markets have capitulated," wrote Nathan Peterson, director of derivatives research and strategy at the Schwab Center for Financial Research (SCFR), late last week. "We are registering higher closes. The VIX is still elevated, but it isn't extreme."

Three things to watch

- What jobs report means for rates: Mixed signals from Friday's nonfarm payrolls report—weaker wage growth and downward revisions to prior reports accompanied a strong March headline reading and falling unemployment—received a hawkish read from the futures market. Chances of at least one rate hike at some point this year climbed to 7% soon after the data, from 0.2% on Thursday, according to the CME FedWatch Tool. Odds of that rose to 9% this morning. Chances of a pause later this month remained 99%, while chances of a rate cut this year fell to 12% early today from about 23% on Thursday. Schwab's experts still expect an extended rate pause. The large March gain followed a sharp February drop and a strong January increase. Jobs growth year to date averaged 68,000 per month, about half the level seen over the full year of 2024 but a better showing than 2025, assuming this level continues. And while unemployment fell to 4.3% last month from the previous 4.4%, there's a chance the "improvement" could reflect fewer people looking for work—not a bullish sign for the economy. Labor force participation remains light, and the government doesn't count people as "unemployed" if they've stopped seeking jobs.

- Slower wage growth—healthy or harmful for margins? March average hourly wages rose a less-than-expected 0.2% monthly and 3.5% year over year. The annual growth was the lowest since May 2021. At some point, softer wage growth and higher non-discretionary costs, such as gas, could hurt consumer demand, if the war continues. Slowing wage growth might reflect fewer job openings, a smaller number of employees leaving their jobs, and a shift in jobs growth away from traditionally higher-paying positions. Jobs growth in the financial sector fell and business and professional services growth flattened in March—two of the higher-paying areas. Slower salary boosts would be positive for inflation, productivity, and in some respects margins, particularly at firms that don't sell directly to consumers. It would likely be tough for companies dependent on consumer spending. Even as consumers face lower wage growth that could tighten their wallets, companies face higher wholesale costs but might have less pricing power with consumers reticent. That could mean a weaker earnings growth set-up for consumer discretionary and consumer staples firms. Still, one month isn't a trend, and, fair or not, most consumer spending comes from the top 20% of earners who may not be hurting.

- Cautious optimism pervades: The Cboe Volatility Index (VIX) climbed 4% to near 25 early today, a possible caution sign that contrasts with slight gains in stocks and a sign the overall market maintains a bearish tilt despite last week's slight rebound. In other signs of caution early today, Treasury yields pivoted around 4.35% for the 10-year note this morning ahead of key auctions tomorrow and Wednesday for 3-year and 10-year notes. Auctions last month drew lackluster demand. With yields steady, VIX up, and crude near $110, the overall market could remain cautious despite some optimism on the war front. Technically, the S&P 500 Index remains well below its 200-day moving average of 6,644. So long as crude remains above $110 and the index stays below that 200-day level, it's hard to say the market has truly turned around from its March slump.

To get the Schwab Market Update in your inbox every morning, subscribe on Schwab.com.

On the move

- Crypto-related stocks including Strategy (MSTR) and Coinbase (COIN) rallied 4% and 3%, respectively, early Monday, in line with a 4% gain for bitcoin (/BTC). Sometimes rallies in bitcoin signal risk-on sentiment in the market.

- Netflix (NFLX) rose 1.8% in early trading following a Goldman Sachs upgrade to buy from neutral. Goldman believes Netflix earnings later this month will show a strong start to 2026.

- Semiconductor stocks Intel (INTC) and Micron (MU) added 2% and 3%, respectively, early Monday, lifted by analyst reports that chip prices are rising amid shortages brought about by heavy demand.

- Twilio (TWLO) added 3.3% today upon getting upgraded to buy from hold at Jefferies, which cited its greater conviction in the role Twilio will play in the voice AI tech stack.

- Dow (DOW) slipped 3% after a downgrade from Bank of America, which now rates the stock at underperform. The firm is downgrading a trio of petrochemical stocks following strong year-to-date share price performance driven by what it believes to be "unsustainable market tailwinds."

- Soleno Therapeutics (SLNO) climbed 33% early today after an announcement that Neurocrine Biosciences (NBIX) has entered into a definitive agreement to acquire Soleno for $53 per share in cash, representing a total transaction value of $2.9 billion. Neurocrine made the move to solidify its endocrinology and rare disease portfolio, the company said in a press release.

- Tesla (TSLA) plunged more than 5% last Thursday after the EV maker reported a 14% drop in vehicle deliveries versus last quarter. Increasing competition, the loss of federal EV tax credits last fall, and a challenging car sales market have hindered Tesla in recent quarters.

- Shares of the optical networking and AI infrastructure players Lumentum (LITE) and Ciena (CIEN) both surged more than 7% Thursday as investors continued to speculate that AI data center spending will drive demand for fiber optics and networking equipment.

More insights from Schwab

Sector views: Each month, the Schwab Center for Financial Research provides an update view of each sector. Check the April ratings as industrials and health care are most favored, with real estate and consumer discretionary least favored.

Screening for value: The Stock Screener on schwab.com is a tool for finding stocks that meet specific criteria, including value stocks. Learn how to use it to find stocks that meet your own criteria.

Sunk costs insight: Why do people keep investing time and money into something even when future benefits no longer justify continuing? In the latest Schwab Choiceology podcast with Katy Milkman, she explores the sunk cost fallacy and how it can skew our judgment.

Chart of the day

Nasdaq

Though major indexes like the S&P 500 Index and the Nasdaq-100® remain in downtrends below key trend-lines on the charts, the PHLX Semiconductor Index (SOX—candlesticks) last week emerged from a short span below its 100-day moving average (blue line), which is "incrementally bullish from a near-term technical perspective," said Peterson, of SCFR, in his latest Weekly Trader's Outlook.

The week ahead