Stocks Retreat, Oil Climbs Awaiting Iran Deadline

Published as of: April 7, 2026, 9:15 a.m. ET

Listen to this update

Listen here or subscribe to the Schwab Market Update in your favorite podcast app.

| The markets | Last price | Change | % change |

|---|---|---|---|

| S&P 500® Index | 6,611.83 | +29.14 | +0.44% |

| Dow Jones Industrial Average® | 46,669.88 | +165.21 | +0.36% |

| Nasdaq Composite® | 21,996.34 | +117.16 | +0.54% |

| 10-year Treasury yield | 4.33% | Unch | -- |

| U.S. Dollar Index | 99.91 | -0.07 | -0.07% |

| Cboe Volatility Index® | 25.47 | +1.31 | +5.42% |

| WTI Crude Oil | $114.92 | +2.49 | +2.22% |

| Bitcoin | $68,505 | -$1,440 | -2.13% |

(Tuesday market open) Tonight marks President Trump's deadline for Iran to re-open the Strait of Hormuz, and stocks fell early as tension grew. Crude oil—now near $114 per barrel—could set the pace for stocks, with data and earnings sparse. The market remains on tenterhooks as ceasefire hopes flagged and Trump threatened to destroy Iran's infrastructure starting at 8 p.m. ET if the strait stays closed.

Back home, Treasury auctions might draw attention with 3-year notes on the block today. Results from this and a 10-year note auction tomorrow could move yields, which rose last month when demand faltered and raised concerns that investors might be less bullish on U.S. assets. "Sticky inflation, fiscal concerns, and rising global bond yields all suggest the 10-year Treasury yield will hold above 4% for the time being," said Collin Martin, head of fixed income research and strategy at the Schwab Center for Financial Research (SCFR). Yields flattened near 4.33% early after the government reported a much worse-than-expected 1.4% monthly drop in February durable goods orders.

Major indexes advanced Monday in a low-volume rally that lifted eight of 11 S&P 500 sectors. The S&P 500 Index posted its fourth straight gain. The slow post-holiday trading, however, might signal lack of conviction, meaning yesterday's rally could be discounted to some extent. In a new development, the U.S. and Israeli militaries conducted strikes on Iran's Kharg Island—a strategically vital oil site—early today, Bloomberg reported. Vice President JD Vance posted that the strikes don't represent a change in strategy, but the news appeared to push stocks lower. Other media outlets reported that negotiations continue.

Three things to watch

- Q1 EPS growth seen up at 13.2%: With Delta Air Lines (DAL) reporting early tomorrow before earnings kick off in earnest next week, it's worth pondering FactSet's most recent estimates. It pegged first quarter S&P 500 earnings per share growth at a healthy 13.2%, up from the previous 13% estimate. FactSet expects 10 of 11 sectors to report year-over-year earnings growth in the first quarter, led by technology. Only energy is expected to be red. Analysts pencil in accelerating earnings growth later this year, though there's debate about how rising energy costs could affect that. A slowdown in U.S. economic growth due to costly gas might work its way into corporate growth, as well. The Atlanta Fed's GDPNow meter for the first quarter fell to just 1.6% late last week. Guidance from reporting companies this month could bring more clarity on whether analysts are too positive or about right on EPS growth, a major determinant of stock values. First quarter earnings accelerate next week, starting with Goldman Sachs (GS) on Monday.

- Volatility watch continues: Today is the first anniversary of "VIX-apocalypse" when the Cboe Volatility Index (VIX)—sometimes called the "fear index"—doubled overnight to 60 amid confusion and anxiety following "tariff liberation day." Today, VIX is near 25 despite circumstances that a year ago might have seemed even more severe than Trump's tariffs—which could be lifted at a whim. The Strait of Hormuz can't be opened by putting pen to paper. Nevertheless, the fierce hedging that characterized the first two to three weeks of March as investors built a cautious stance due to the war and oil eased somewhat as the old month ended and April began. Hedging activity remains historically high but down from a month ago, with some institutions pulling back on hedges amid a slight positive sentiment change on the institutional side. Some of the move could reflect technical factors, and investors remain bearish overall. That said, they haven't taken much money off the table. Instead, they seem to be moving into more diversified products. And the VIX futures complex projects slightly lower volatility the rest of the year. This might seem arcane, but VIX can be a useful directional indicator for major indexes.

- Retail investors pulled back in March: Schwab clients turned slightly bearish in March as war raged in Iran, sending the Schwab Trading Activity Index (STAX) down 2.23% from February's long-term high. However, last month's headline STAX reading of 56.04 was still the highest for any recent month other than February. As markets retreated in March, Schwab clients appeared to spend less time trying to pick individual names, concentrating instead on diversified exchange-traded funds (ETF). Five of the top 10 highest names in terms of client net-buys during March were ETFs, not individual stocks. Rather than attempting to identify individual standout opportunities, investors are adopting a broader, less concentrated strategy and seeking to diversify risk through investments in more diversified ETFs, something not seen to this degree in some time. Checking individual stocks, clients tracked by STAX made Nvidia (NVDA) the biggest in terms of monthly inflows for an individual company last month, followed by Microsoft (MSFT), Tesla (TSLA), Micron (MU), and Amazon (AMZN). The names with the most net outflows in March were Broadcom (AVGO), Netflix (NFLX), Advanced Micro Devices (AMD), and two new names to the list, Circle Internet Group (CRCL) and Occidental Petroleum (OXY).

To get the Schwab Market Update in your inbox every morning, subscribe on Schwab.com.

On the move

- Humana (HUM), UnitedHealth Group (UNH), and CVS (CVS) climbed sharply early today, with Humana up 11%. The Centers for Medicare and Medicaid Services (CMS) released its 2027 Medicare Advantage and Part D rate announcement, which analysts said improved significantly for the health industry. Wells Fargo raised its price target on Humana, saying the Medicare Advantage final rule makes the analyst more confident Humana can improve margins.

- Broadcom got a 3% boost early today on news that the chip designer agreed to expanded chip deals with Alphabet (GOOGL) and Anthropic that will include Broadcom developing Google's custom AI chips, Reuters reported.

- Delta descended 1.3% early ahead of its earnings tomorrow morning. Results could draw attention amid surging jet fuel prices even after the OPEC cartel yesterday promised to hike output next month. Consensus is for Delta to post earnings per share of $0.61, a 33% year-over-year increase.

- Arm Holdings (ARM) shed 3.5% ahead of the open following a downgrade by Morgan Stanley to equal weight from overweight. The analyst said Arm's transition into chip making will take time to ramp commercially, with near-term execution risks.

- Most Magnificent Seven and semiconductor stocks dropped ahead of the open, sometimes a sign of risk-off sentiment. Nvidia and Tesla each fell 1% or more. Tesla is down 22% year to date.

- Paramount Skydance (PSKY) climbed almost 3.6% Monday, helped by a Wall Street Journal report that the company has received signed equity commitments of close to $24 billion from three sovereign wealth funds led by Saudi Arabia to help back its takeover of Warner Bros. Discovery (WBD).

- The average option-adjusted spread of high-yield corporate bonds fell below 3% for the first time since early March. "The drop may indicate relative resilience of the economy and corporate fundamentals heading into the war," said my colleague Martin, while adding there may not be much further downside to spreads considering the potential spillover risk from private credit markets.

- The rate outlook grew slightly more hawkish following last Friday's March nonfarm payrolls report showing jobs growth of 178,000 that almost tripled expectations. Odds of a rate cut or a rate hike this year were evenly divided as of early today at about 10% each, according to the CME FedWatch Tool. There's a 79% chance that rates stay paused all year.

- Technically, the S&P 500 Index remains well below its 200-day moving average of 6,647. However, yesterday's close looked positive, as the index rose in the final minutes to finish near its intraday high. Investors appear to want protection in case things get worse in the Gulf, but also apparently want to keep money in the market in case a ceasefire occurs.

More insights from Schwab

Not just gasoline: While crude oil spikes often put the focus on gas prices, an oil price shock can raise prices for all kinds of products ranging from contact lenses to disposable diapers. Learn more about how rising crude might affect the U.S. economy and how to track how crude price increases work through supply chains in Schwab's new look at commodities.

Crypto allocation considerations: Investors thinking of adding cryptocurrencies to their portfolios might want to consider two possible approaches and beware of possible volatility, said Jim Ferrarioli, director of digital currencies research and strategy, SCFR, in his newest look at crypto investing.

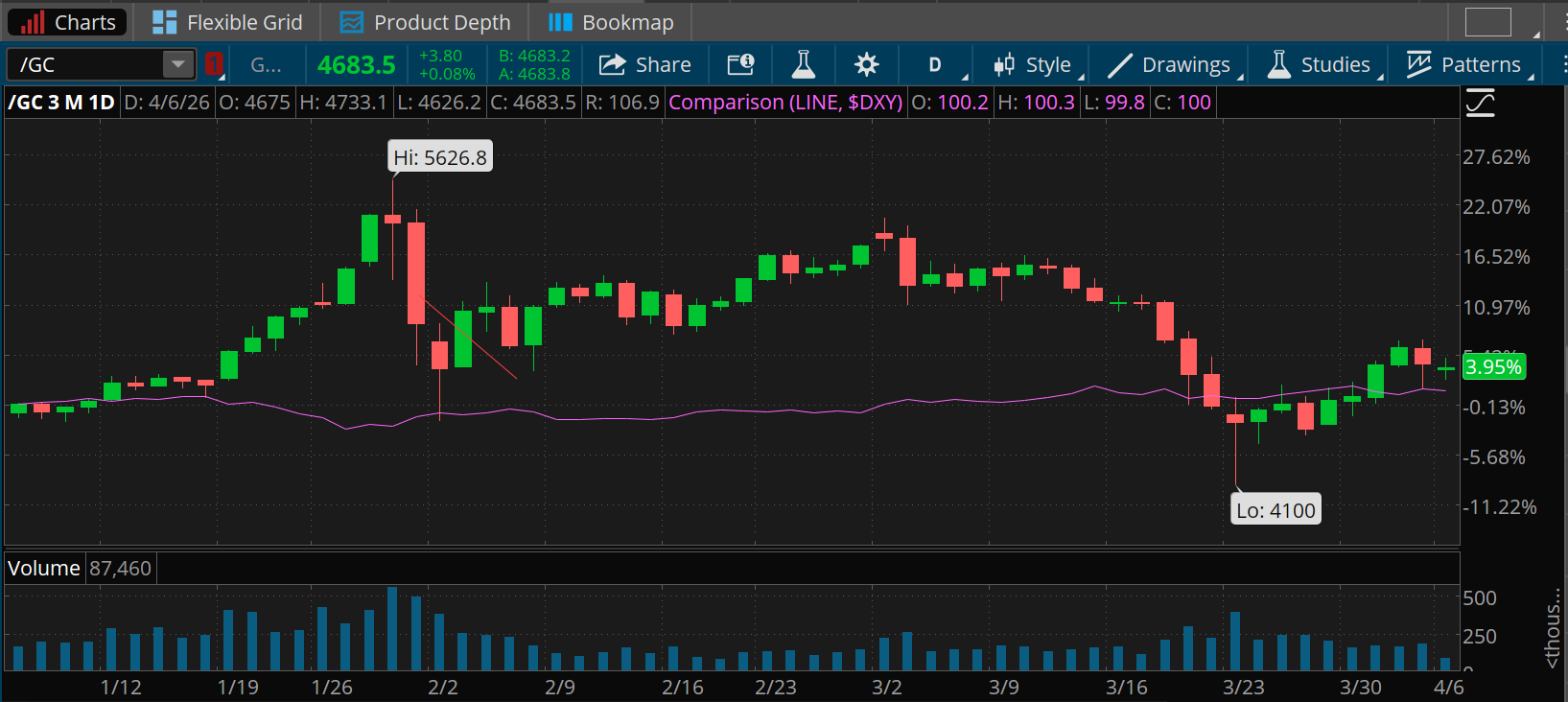

Chart of the day

ICE, CME Group

Though gold often divorces itself from the dollar, the two had similar performances in the first quarter. Gold (/GC—candlesticks) is up around 4% and the U.S. dollar index ($DXY—purple line) is up about 1%. Though gold spiked to all-time highs in early February, it lost ground once the war began, while the dollar rose. Typically, gold is seen as an inflation hedge while the dollar tends to lose value when inflation threatens, but the war appears to have temporarily changed that dynamic.

The week ahead

Check out the investors' calendar for a summary of the top economic events and earnings reports on tap this week.

April 8: Expected earnings from Delta Air Lines (DAL), Constellation Brands (STZ), and Applied Digital (APLD).

April 9: Fourth quarter GDP-third estimate, February PCE prices.

April 10: March CPI, March core CPI, preliminary April University of Michigan Consumer Sentiment.

April 13: Expected earnings from Goldman Sachs (GS), March existing home sales.

April 14: March PPI, March core PPI, and expected earnings from JPMorgan Chase (JPM), Johnson & Johnson (JNJ), Wells Fargo (WFC), Citigroup (C), BlackRock (BLK).