Power and AI Boost Infrastructure Investments

Key points:

- A number of long-term, or secular, drivers are creating potential opportunities for infrastructure operators and builders.

- Infrastructure companies can be both defensive and cyclical in nature. Infrastructure operators feature high barriers to entry and relatively stable growth and dividends, while builder-related companies are seeing opportunities from multi-year capital investment cycles tied to the increased demand for power due to electrification, use of artificial intelligence (AI), and the need to modernize aging infrastructure.

- Infrastructure companies are not without risks, which can include regulatory changes, fluctuations in capital availability, rising input costs, supply-chain disruptions, and raw-material and energy shortages (such as those emanating from the U.S.-Israel war in Iran). Technological changes can also alter the outlook for infrastructure investment.

Infrastructure companies are seeing opportunities from several longer-term, secular themes playing out across the global economy. There are two broad types of infrastructure companies: operators and builders. Operators tend to be more defensive in nature, given their exposure to long-lived assets, high barriers to entry, and relatively less sensitivity to cyclical conditions and inflation. Builders are often more growth oriented and cyclical in nature, due to their exposure to broader capital spending (capex) trends and economic developments.

Infrastructure operators are relatively defensive

Infrastructure owners and operators, including those in charge of utilities, toll roads, ports, airports, as well as energy pipeline and terminal operators, tend to have several defining characteristics that may insulate them from swings in economic cycles, such as:

- Recession resistance. They provide essential services that remain in demand, even during economic slumps.

- Competitive advantage. High barriers to entry and regulatory complexity create competitive advantages, or moats, that protect long-term profits and market share from competition. Their long life physical assets tend to be costly and time consuming to replicate and do not become obsolete quickly and are sometimes referred to "Heavy Asset, Low Obsolescence" (HALO) businesses.

- Inflation protection. These companies often operate under regulated frameworks or long-term contracts that explicitly or implicitly allow for inflation pass-through via rate-based adjustments, inflation linked fees, and power-purchase agreements. These features allow revenues to adjust with rising prices. However, margins may still be pressured if input costs rise faster and earlier than allowed price increases.

- Dividend income. Many infrastructure companies tend to generate relatively stable cash flows, which may support consistent dividend payouts. Investors may find this an attractive feature during periods of market turbulence.

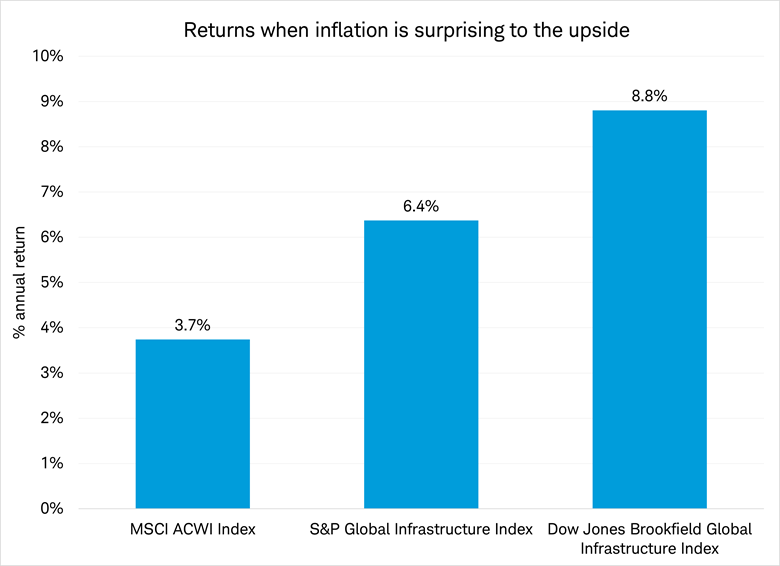

Infrastructure performs better when inflation is surprising to the upside

Source: Charles Schwab, Bloomberg, MSCI, S&P Global data as of 4/8/2026.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

High inflation is defined periods where the U.S. consumer price index (CPI) is higher than the consensus. The reference period is December 2003 through February 2026. The S&P Global Infrastructure Index is designed to track 75 companies from around the world chosen to represent the listed infrastructure industry while maintaining liquidity and tradability; the index includes three distinct infrastructure clusters: energy, transportation, and utilities. The Dow Jones Brookfield Global Infrastructure Index is designed to measure the performance of pure-play infrastructure companies domiciled globally.

Although infrastructure operators have defensive characteristics, they are not immune to trends in economic activity. Should economic growth moderate, usage based revenue sources, such as tolls, airport revenue-sharing or energy demand, could slow. Additionally, these capital-intensive businesses could have difficulty accessing new funding if credit conditions tighten during an economic slowdown. Other risks include regulatory and political pressures: the potential for price controls, windfall taxes, or other government directives aimed at addressing consumer affordability. Cybersecurity risks aimed at infrastructure are an additional consideration.

Growth in electrical demand and related infrastructure

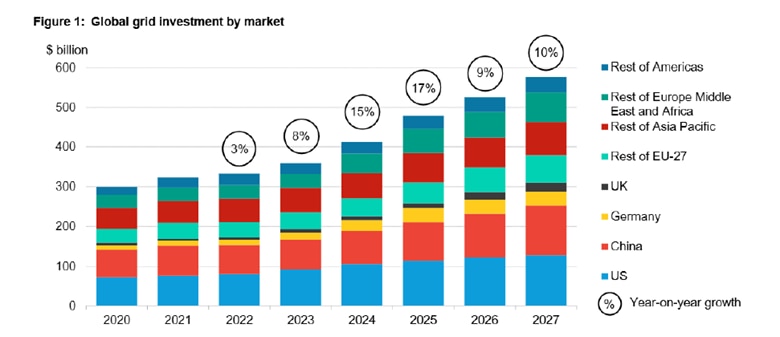

Structural forces are converging to support a multi year investment cycle in power infrastructure, which could benefit builder-related companies. Power grids are under strain due to growth in the use of artificial intelligence (AI), changing weather patterns increasing the peak usage for both cooling and heat, and increased ownership of electric vehicles. The strain could be compounded by an aging infrastructure in need of modernization, including additional load balancing technologies, or long duration storage. Residential and commercial buildings are shifting to more energy-efficient heat pumps that use electricity instead of fossil-fuel burning furnaces, adding strain on electrical utilities. Investment in the electrical grid has accelerated in recent years due to the increased demand for power, according to BloombergNEF, as seen in the chart below.

Global grid investment

Source: Bloomberg. NEF, Grid Investment Outlook 2025, published in December 2025.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Some data in the “rest of” regions, which represent 20% of the global total, is modeled by BNEF.

AI development seems to be turbocharging electricity demand by data centers—first to train large language models (LLMs) to recognize patterns, then later to use those models to make near real-time predictions using unseen information and draw conclusions during the AI inference phase. Training builds the models, while inference puts them to work continually. Demand for power in both AI phases is expected to continue to grow, as seen in the chart below.

Data centers require increased power

Source: McKinsey Data Center Demand Model published in December 2025.

*All years are estimated. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Concurrently, geopolitical disruptions have continued to expose vulnerabilities in global energy supply chains, reinforcing incentives for onshoring, reshoring, and diversifying access to critical energy and commodity supplies. Governments are increasingly funding infrastructure upgrades to improve economic efficiency and reduce vulnerabilities, illustrated by Germany's landmark infrastructure fund introduced in 2025, allocating 500 billion euros over 12 years.

Infrastructure investments are not without risks. In the near term, supply chain disruptions related to war, tariffs, and manufacturing dislocations could raise construction costs or create material shortages. Supply constraints of energy, commodities, water, chemicals, or specific components like microchips could limit overall growth. Operational challenges can also be a risk; labor shortages, land access, and permitting issues can cause disruptions to specific projects or entire sub-industries. Changes in regulations and consumer attitudes may be potential roadblocks to project launches or completion.

Longer-term uncertainties include technological innovations that could change data center requirements, such as advances in quantum computing that reduce energy per task, potentially altering demand and capital spending trajectories over time. Companies in the renewable energy industry may face pressure on profit margins due to potential competition from exporters that are subsidized by the Chinese government.

How investors can access infrastructure plays

Investors can find both individual companies and mutual funds or ETFs that focus on infrastructure. Infrastructure funds generally allocate to industries across the following sectors to varying degrees:

- Sector

- Infrastructure-related industries

-

SectorUtilitiesInfrastructure-related industriesElectric, gas and water, and independent power producers

-

SectorIndustrialsInfrastructure-related industriesEngineering and construction services and equipment; electrical components and equipment (generators, inverters, metering equipment, regulators, transformers, fiber optic components, regulators, cables, etc.); and transportation assets (toll roads, airports, and ports)

-

SectorEnergyInfrastructure-related industriesOil and gas storage and transportation, pipelines, and liquified natural gas (LNG) terminal operators

-

SectorMaterialsInfrastructure-related industriesSteel, aluminum, copper, cement, and aggregates

Some funds also include information technology companies that provide data center equipment and related components. This exposure may add more growth potential but also more market-related volatility to the investments. Strategies may emphasize asset owners and operators or tilt more heavily toward the companies focused on infrastructure buildouts. Investors can also choose between U.S. focused and globally diversified approaches, with the latter introducing foreign exchange considerations tied to movements in the U.S. dollar.

Takeaway

Infrastructure presents a unique opportunity to invest in secular themes such as electrification and use of AI to meet increased power demands, as well as upgrading outdated physical assets. By combining the defensive and income-generating characteristics of infrastructure operators with growth-oriented infrastructure builders, investors may be able to build a balanced asset to add to their portfolios. Although these companies are not immune to a potential economic slowdown, they may provide a longer-term investment opportunity amid an uncertain macroeconomic backdrop.

Heather O'Leary, Senior Manager, Equity Research and Strategy, contributed to this report.