Weekly Trader's Outlook

Stocks Rally to Fresh Highs, Buoyed by Strong Earnings, Middle East Ceasefire Hopes

The Week That Was

If you read last week's blog, you might recall that I had a "Cautious" outlook for stocks this week, noting the cycle-high yield in the 30-year and uncertainty around the trajectory of oil prices. Stocks rallied to fresh all-time highs this week (sans the Nasdaq), which was set off at the start of the week by a drop in both oil prices and Treasury yields, after Treasury Secretary Scott Bessent suggested a ceasefire with Iran was near, so my "cautious" forecast turned out to be wrong. However, the falling oil prices and yields were the risks I identified to my forecast - there is just no way to use any indicator to predict these developments given the volatile news flow around the Iran conflict. As for the potential deal, nothing has been officially announced, though Iran said a deal with Oman to reopen the Strait of Hormuz is "on the verge of being finalized". Even though a deal has yet to be reached, WTI crude prices are down 7.7% on the week (WTI Sep futures were last seen trading up $0.83 to $78.11/barrel), which is likely why equity investors were willing to push stocks to fresh highs this week.

Although the Nasdaq is not at new highs like the other majors, tech stocks continued to rebound, initiated by both last week's collapse of hedge fund Situational Awareness (capitulation event) coupled with evidence of AI monetization & forecasted growth acceleration from both Microsoft and Amazon. Palantir's solid "beat and raise" quarter on Monday also helped boost sentiment around software and the entire AI cohort. Lastly, after consolidating within a trading range of roughly 7,250-7,600 for three months, the S&P 500 index broke out to fresh all-time highs on Wednesday. In my view, in addition to the incremental bullish technical development, when the SPX breaks out to fresh all-time highs, additional buying pressure can result from both a) performance chasing by fund managers and b) short covering.

Tracking the Q2 earnings scorecard, the results continue to be very strong, even when removing one-time earnings contributions due to investment gains from Amazon, Alphabet and Microsoft. So far, 442 of the S&P 500 companies have reported results and 69% have beat estimates on the top line while 87% have beat on the bottom line. Perhaps more impressively EPS growth is currently tracking at 51.44% and revenue growth is at 14.70%. When excluding one-time investment gains, the EPS growth rate for the S&P 500 is tracking 26-29% (according to estimates from Goldman Sachs and data compiled by LSEG).

Outlook for Next Week

At the time of this writing (2:20 PM ET) stocks are higher across the board, though off the highs of the day (DJI + 49, SPX + 30, $COMP + 243, RUT + 28), driven by this morning's soft jobs report, which cools the rate hike fears some and encourages higher prices in risk assets. Last week 30-year Treasury yields were hitting fresh cycle highs and yields on the 10-year were hitting 20-month highs, but yields pulled back across the curve this week, along with oil prices. While we still don't have any news of a deal between the U.S. & Iran, oil prices and yields are behaving as if the probability of one is high. Looking to next week, we'll get the monthly inflation reports (CPI/PPI) and there will be several important earnings reports from the AI complex (ex. AMAT, CSCO, CRWV, LITE, NBIS). From a technical perspective, one could say we are overbought on a very-near term basis given the strong week, but the momentum is to the upside. The "pain trade" is also higher, given that some performance chasing may still be lurking underneath the surface. Yes, the Iran war is a wild card, and yes August is not a strong month for stocks from a seasonal factor, but I believe the outlook favors the bulls due to a) bullish technicals/momentum b) potential performance chasing and c) potential short covering. Therefore, I am providing an overall "Moderately Bullish" forecast for stocks next week. What could challenge my forecast? Since we are overbought on a very near-term basis, its possible we consolidate next week, or it's even possible that the SPX does a technical "check back ", which means the index would go back to test the prior resistance level around 7,600.

Other Potential Market-Moving Catalysts

Economic:

- Monday (8/10): no reports

- Tuesday (8/11): Existing Home Sales

- Wednesday (8/12): Consumer Price Index (CPI), EIA Crude Oil Inventories, MBA Mortgage Applications Index, Treasury Budget

- Thursday (8/13): Producer Price Index (PPI), Continuing Claims, EIA Natural Gas Inventories, Initial Claims

- Friday (8/14): Business Inventories, University of Michigan Consumer Sentiment

Earnings:

- Monday (8/10): Aaon (AAON), AECOM (ACM), Apogee Therapeutics (APGE), AST SpaceMobile (ASTS), Axsome Therapeutics (AXSM), Barrick Mining Corp. (B), California Resources Corp. (CRC), Camtek (CAMT), Embraer SA (EMBJ), Ferguson Enterprises (FERG), Rocket Lab Corp. (RKLB), Simon Property Group (SPG), YPF SA (YPF)

- Tuesday (8/11): Aramark (ARMK), Cardinal Health (CAH), CAVA Group (CAVA), CoreWeave (CRWV), Elbit Systems (ESLT), Franco-Nevada Corp. (FNV), Hims & Hers Health (HIMS), Lumentum Holdings (LITE), Middleby Corp. (MIDD), On Holding (ONON), Quantinuum (QNT), Sea Ltd. (SE), Super Micro Computer (SMCI), Venture Global (VG)

- Wednesday (8/12): Amcor PLC (AMCR), Brinker International (EAT), CAE Inc. (CAE), Cerebras Systems (CBRS), Cisco Systems (CSCO), Coherent Corp. (COHR), EnerSys (ENS), Korea Electric Power Corp. (KEP), Navan Inc. (NAVN), Nebius Group (NBIS), Pan American Silver Corp. (PAAS), Performance Food Group (PFGC)

- Thursday (8/13): Applied Industrial Technologies (AIT), Applied Materials (AMAT), Ascendis Pharma (ASND), Brookfield Corp. (BN), Celcuity Inc. (CELC), Credicorp (BAP), Dillard's (DDS), DLocal Ltd. (DLO), JD.com (JD), Nu Holdings (NU), QXO Inc. (QXO), StoneCo Ltd. (STNE), Tapestry (TPR), X-Energy (XE)

- Friday (8/14): Anteris Technologies Global Corp. (AVR), Arrivent Biopharma (AVBP), ASP Isotopes Inc. (ASPI), Avalyn Pharma (AVLN), Hemab Therapeutics Holdings (COAG), RLX Technology (RLX), United State Antimony Corp. (UAMY)

Economic Data, Rates & the Fed

There was a heavy dose of economic data this week, which was highlighted by several readings on the state of the labor market. On the whole, the data was soft, but not dramatically so, since there was impact due to the World Cup and private payroll growth remained relatively stable. The tepid payroll growth, coupled with weak wage growth, helped temper the outlook on inflation and the probability of a Fed rate hike pulled back this week. Elsewhere, manufacturing and services PMI data remained healthy and expansionary territory. Here's a breakdown of the reports:

- Nonfarm Payrolls: Headline unexpectedly declined by 23,000 in July, which was well below the +80,000 economists were expecting. Additionally, June payrolls were revised down to +20,000 from the initial report of +57,000 and May was revised lower by 66K). However, if you focus on just private payroll growth, there was payroll growth of 30K in July, which was the same as last month.

- Unemployment Rate: Ticked down to 4.1% from 4.2% in the prior month and 0.1% below estimates. However, the drop in the Unemployment Rate was driven by a relatively larger decline in the labor force participation rate.

- Average Hourly Earnings: Average hourly earnings increased just 0.1% month-over-month, which was below the +0.3% economists were expecting. On an annualized basis, average hourly earnings are up +3.2%, well below the +3.5% expected.

- U.S. Labor Force Participation: Dropped to 61.4% in July, which represents the lowest reading in over five years.

- Average Workweek: 34.3 versus 34.3 expected.

- ADP Employment Change: U.S. private employers added 44K jobs in July, which was a slowdown from the 95,000 added in the prior month, and below the +80K Briefing estimate. Virtually all the gains came from healthcare-related sectors.

- JOLTs-Job Openings: Eased modestly to 7,357,000 in June from 7,537,000 from the prior month, and below the 7.40M economists were expecting.

- ISM Non-Manufacturing Index: Increased slightly to 54.1% in July from 54.0% in June, remaining firmly in expansionary territory (> 50.0) for the 25th consecutive month. The Prices Index increased to 70.3 in July from 67.7 in June. The 12-month Prices average increased 0.1% to 68.1, which is the highest since April 2023.

- S&P Global U.S. Services PMI: Increased to 54.6 in July from 51.2 in June, which represents the highest reading in nine months.

- ISM Manufacturing Index: Increased to 55.6% in July from 53.3% in June, remaining in expansionary territory for the seventh consecutive month. This represents the highest Manufacturing PMI reading since May of 2022. The Prices Index decreased to 71.1% in July from 73.0% in June but remains in expansion or "increasing" territory.

- S&P Global U.S. Manufacturing PMI: Remained unchanged at 53.9 in July from the prior month. Chief Business Economist at S&P Global Market Intelligence Chris Williamson stated, "Although the headline PMI held steady in July, beneath the survey we see some warning signs about the future growth trajectory. Production rose at a markedly slower rate in July, linked to a third month of weakness growth of new business, in turn reflecting reduced inventory building after the especially strong precautionary stock accumulation reported in Q2".

- Productivity-Preliminary: 1.4% vs. 0.5% est.

- Unit Labor Costs: 1.3% vs. 1.5% est.

- Factory Orders: -0.3% vs. +0.3% est.

- Construction Spending: -0.1% vs. 0.4% est.

- EIA Crude Oil Inventories: +2.48M barrels.

- EIA Natural Gas Inventories: +33 bcf.

- Initial Jobless Claims: Initial applications for US jobless benefits increased 1K from last week's (upwardly revised) 198K to 199K. Continuing Claims increased by 24K from the prior week to a seasonally adjusted 1.801M.

- The Atlanta Fed's GDPNow initial "nowcast" for Q3 GDP was revised up to 5.8% from 5.0% last week, primarily driven by an increase in consumer spending and private inventories estimates.

U.S. Treasury yields moved lower across the board this week which resulted in some slight steepening of the yield curve. Hope for a deal with Iran, lower oil prices and soft job growth all contributed to lower yields. Compared to last Friday, 2-year Treasury yields are down ~9 basis points (4.201% vs. 4.291%), 10-year yields are also down ~9 basis points (4.652% vs. 4.745%) while 30-year yields decreased ~7 basis points (5.203% vs. 5.275%).

Market expectations around a potential rate hike from the Federal Reserve fell this week, driven by hope for an Iran deal, lower oil prices and relatively soft jobs data. Per Bloomberg, the probability of a Fed rate hike at the September FOMC was 71% last Friday, fell to 64% on Monday (lower oil prices, Iran deal hopes), and id down to 42% today following this morning's Nonfarm Payrolls report. The first theoretical 100% probability of a rate hike has been pushed out to December from October last week.

Technical Take

S&P 500 Index (SPX + 36 to 7,746)

The S&P 500 Equal Weight (SPXEW) broke out to fresh all-time high this week, and as I mentioned in the opener, not only is this technically bullish, but the move tends to attract extra buying pressure from a) performance chasing by fund managers and b) short covering. Looking at the chart, we've got a bullish cross in the MACD indicator and the last 5 trading days looks akin to a bull flag (if so, it's not yet confirmed until a fresh high, either on an intraday or closing basis, is made). If the index were to pullback, look for the prior high around 7,600 to be a key support level, but otherwise the near-term technicals look bullish to me.

Near-term technical translation: bullish

Source: ThinkorSwim trading platform

Past performance is no guarantee of future results.

Nasdaq Composite Index ($COMP + 256 to 26,605)

The relatively lagger, the Nasdaq Composite index ($COMP), is on track to be up over 6% this week, driven by a continuation from last week's revival in the AI complex. The rebound, which started last Thursday, was driven by a selling crescendo event (Situational Awareness collapse) plus stellar earnings reports, which showed evidence of AI monetization traction, from both MSFT and AMZN. The $COMP is not back above its 50-day SMA, which is incrementally bullish, and is currently 2.20% beneath its all-time high of 27,190 from early June. There "could" be some resistance we are up against around 26,600-26,700 (the highs from mid-May and mid-June), but otherwise the technicals have shift back in favor of the bulls for this index in my view.

Near-term technical translation: moderately bullish

Source: ThinkorSwim trading platform

Past performance is no guarantee of future results.

Cryptocurrencies

The Bitwise 10 Large Crypto Index is up 3% since last Friday, with bitcoin up 3% and ether up 3% at the time of writing. Ethereum Improvement Proposal (EIP)-8361 was submitted earlier in the week, a proposal that impacts staking rewards to reduce ether inflation over time. This led to a selloff in liquid-staking tokens, due to the market perception that their revenue may be impacted from this proposal.

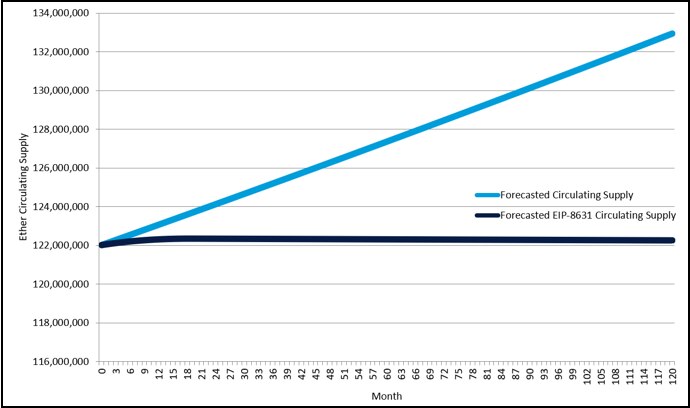

EIP-8361 proposes to reduce net issuance of ether as the staked supply reaches 50% of circulating supply. Through this process, staking yield is expected to decline from approximately 2.6% today to 1.2% over time. As staking yield falls, the burn rate also increases, resulting in ether's supply growth falling from roughly 0.88% per year towards zero.

EIP-8361 would reduce ether's inflation rate to nearly 0%

Source: Glassnode, Schwab as of August 6, 2026.

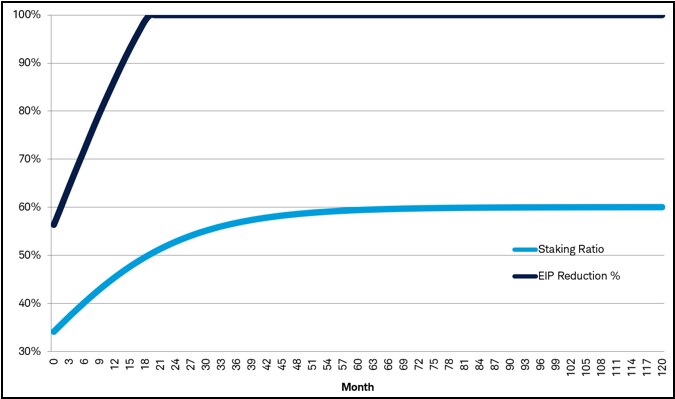

As the staking ratio rises to 50%, 100% of the EIP issuance reduction goes into effect

Source: Glassnode, Schwab as of August 6, 2026.

Upon news of the EIP, Lido Finance (LDO) saw its price fall 15%. The market reaction may reflect concerns regarding future staking yields and protocol revenue. Based on its most recent weekly annualized revenue of approximately $53.9 million, it is currently trading at roughly 5x market-cap-to-annualized revenue, below its historical 25th percentile revenue multiple of 8.3x and well below its historical median multiple of 13.8x. As a result, the key question is not whether EIP-8361 reduces revenue, but whether current valuations already discount a material deterioration in staking economics. Even under an illustrative scenario where protocol revenue declines meaningfully, valuation outcomes may remain supported if revenue multiples normalize toward historical ranges or ETH price appreciation offsets a portion of the reduction in staking rewards.

Protocol revenue is influenced by staking participation, validator yields, fee rates, and ether price. As a result, changes in validator yields do not necessarily translate into equivalent changes in dollar denominated revenue if ether prices appreciate due to reduced supply growth.

LDO is trading at the low end of its historic valuation range

| Historical Revenue Multiple Summary | |

|---|---|

| Minimum Revenue Multiple | 3.4x |

| 25th Percentile Revenue Multiple | 8.3x |

| Median Revenue Multiple | 13.8x |

| 75th Percentile Revenue Multiple | 24.8 |

| Maximum Revenue Multiple | 66.6x |

Investors may be considering three illustrative scenarios regarding EIP-8361 impact to LDO:

- EIP-8361 is adopted and lower staking yields result in a material decline in liquid staking protocol revenue, while valuation multiples remain depressed (25% hypothetical assumption of occurrence).

- EIP-8361 is adopted and lower staking yields negatively impact protocol revenue, but current valuations already reflect much of this risk and revenue multiples normalize toward historical levels over time, supported by a higher ether price resulting from lower net supply growth (25% hypothetical assumption of occurrence).

- EIP-8361 is not adopted and staking economics remain broadly unchanged, allowing valuation multiples to recover from current bear-market levels (50% hypothetical assumption of occurrence).

Under the illustrative scenarios below, the hypothetical assumption of occurrence-weighted valuation outcome exceeds the current implied value

| Scenario | Hypothetical Assumption of Occurrence | Annual Revenue | Revenue Multiple |

|---|---|---|---|

| EIP Not Adopted R-rates | 50% | $53.9M | 10.0x |

| EIP Adopted, Moderate Revenue Impact | 25% | $37.7M | 8.0x |

| EIP Adopted, Severe Revenue Impact | 25% | $26.9M | 5.0x |

Applying the illustrative assumptions shown above results in a hypothetical assumption of occurrence-weighted market cap estimate that is at a premium to LDO's current market cap. Notably, LDO declined approximately 15% following the announcement, which is substantially smaller than the severe downside scenario modeled above. This may suggest investors expect a less severe impact on long-term revenue, some offset from ETH price appreciation, or a lower probability of adoption. Results remain highly sensitive to assumptions regarding protocol revenue, ETH price performance, staking participation, and valuation multiples. Past performance is no guarantee of future results.

Jim Ferraioli, Director of Digital Currencies Research and Strategy, authored this report.

Market Breadth

The Bloomberg chart below shows the current % of members within the S&P 500 (SPX), Nasdaq Composite (CCMP) & Russell 2000 (RTY) that are trading above their respective 200-day Simple Moving Averages (SMA). In short, stocks had a strong up week, and market breadth correspondingly expanded. In fact, SPX market breadth is above January highs. Compared to last Friday, the SPX (white line) breadth improved to 71.74% from 69.73%, the CCMP (blue line) moved up to 47.22% from 44.00%, and the RUT (red line) expanded to 67.01% from 64.03% (all week-over-week).

Source: Bloomberg L.P.

Market breadth attempts to capture individual stock participation within an overall index, which can help convey underlying strength or weakness of a move or trend. Typically, broader participation suggests healthy investor sentiment and supportive technicals. There are many data points to help convey market breadth, such as advancing vs. declining issues, % of stocks within an index that are above or below a longer-term moving average or new highs vs. new lows.

This Week's Notable 52-week Highs (140 today): Amgen Inc. (AMGN + $1.33 to $406.18), Bank of America Corp. (BAC - $0.44 to $62.56), Brinker International Inc. (EAT + $0.08 to $227.35), Metlife Inc. (MET - $1.82 to $98.13), Parker-Hannifin Corp. (PH + $16.68 to $1,086.48), Tapestry Inc. (TPR - $0.90 to $161.10)

This Week's Notable 52-week Lows (74 today): AppLovin Corp. (APP + $9.13 to $344.80), Aptiv PLC (APTV + $2.04 to $48.34), Celsius Holdings Inc. (CELH + $1.00 to $24.77), Group 1 Automotive Inc. (GPI - $1.39 to $269.43), Papa John's International Inc. (PZZA - $0.57 to $24.07), Walker & Dunlop (WD + $0.92 to $45.18)