International

Stay up to date on commentary related specifically to international markets.

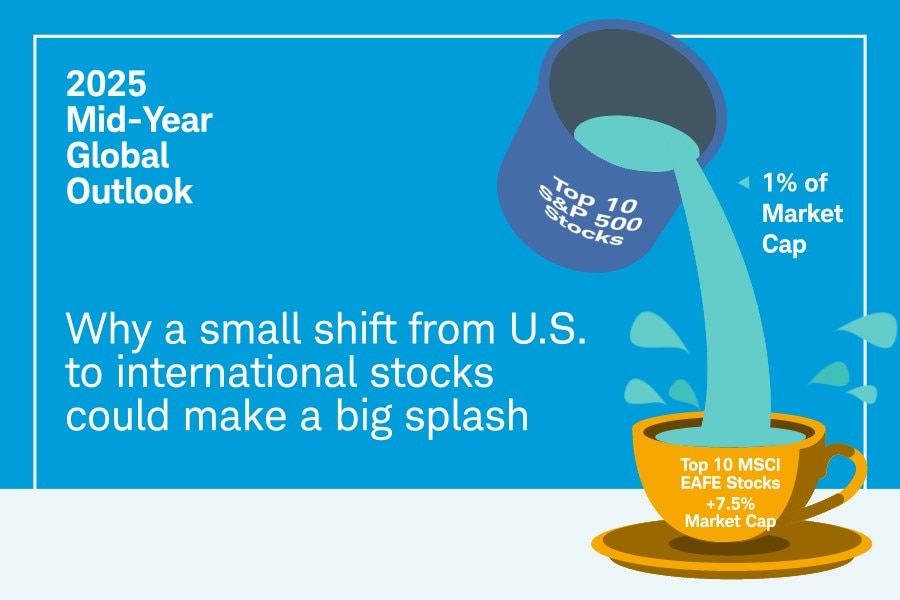

2025 Mid-Year Outlook: Global Stocks and Economy

Investors may revisit international exposure in their portfolios amidst reduced market reactions to tariff announcements, uncertain U.S. policy and lagging U.S. stock performance.

Are Tariffs Over? Court Ruling Isn't the End

Trump's tariffs now face a legal battle. Tariffs may be less arbitrary and reduced in severity or duration, but the next steps are complicated and likely to extend uncertainty.

Weekly Market Outlook

Chief Global Investment Strategist Jeffrey Kleintop's 90-second take on the markets for the week ahead.

Why International and Why Now

The shifting change in market leadership to international outperformance may call for a portfolio review to assess overexposure risks.

Schwab Market Perspective: The Tariff Effect

Stocks have rebounded since the White House delayed steep tariffs that were announced in early April, but trade policy remains a potential driver of volatility.

Tariffs: Q1 Impacts and Q2 Negotiations

A look back at the impacts of tariff announcements last quarter, and what we might expect from tariff negotiations during the 90-day implementation delay in Q2.

Why Is the U.S. Dollar Declining?

Historically the United States dollar strengthens when U.S. Treasury yields rise. But the reverse happened in April after the White House announced widespread tariffs.

Weak Dollar Is No Silver Lining as Firms Face Tariffs

The U.S. dollar hit 3-year lows after tariff "liberation day," and a weak greenback often aids U.S. companies with big overseas sales. That may not happen now as the trade war simmers.

Early Impacts of the Trade War

Theoretical forecasts and earnings announcements may provide initial insights as to the impact of current tariff proposals, although estimates may be imprecise.

Relative Winners in a Trade War

While there are no absolute winners in a trade war, there may be relative winners in the global stock market for investors to consider.